Circle is going public!

And, don't forget, it's tariff day

Welcome to Cautious Optimism, a newsletter on tech, business, and power.

It’s Wednesday and a busy one at that. The biggest news is that Circle has filed to go public, adding another name to the 2025 IPO class. As a stablecoin bull, I’m stoked to get into the S-1 filing (see below).

Today also features the expected 4 PM release of a new, massive wave of trade barriers. Un-Liberation Day is a wildcard, but it appears a safe bet that the world of free trade will dim even more by the evenings.

CO published a short afternoon note yesterday discussing CoreWeave’s share price rebound yesterday, if that’s your sort of thing.

Tesla is expected to release Q1 delivery data today. Analysts expect a drop of about 4% from the car company, with some voices forecasting an even larger drop. We’ll see. Tesla is trading above recent lows in the last week, indicating that at least some investors in the company remain near-term bullish. To work! — Alex

📈 Trending Up: Hypocrisy … AI load … the ‘MAGA’ trade … going indie … digital media subs … getting ‘grokd’ … self-dealing … stagflation? … uh oh …

📉 Trending Down: Revenue at Raspberry Pi … libraries? … penalties for breaking the law … national data …

So much for a data center capacity glut?

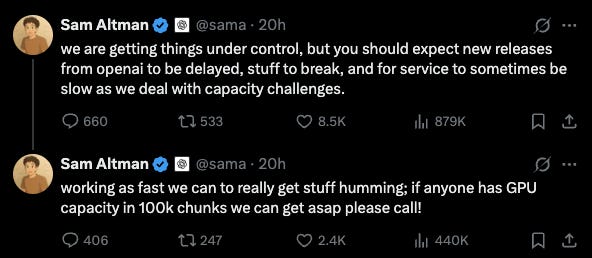

When OpenAI scooped up north of $11 billion worth of GPU capacity from CoreWeave that Microsoft passed on, I wondered: why would a company busy building out what could become the largest compute cluster in the history of the world — the Stargate Project — need to stick its neck out for so much raw processing power over the next five years?

Well, the answer is that OpenAI is GPU constrained today, even with its existing infra deals and partnership with Azure’s parent company. It got pretty damn funny yesterday on the TL.

For reference, if we presume an average retail price of around $30,000 for a Nvidia H100, Sam is looking for “chunks” of capex worth in the neighborhood of $3,000,000,000. That’s a lot of coin.

But more to the point: Consumer demand for new AI tooling can still prove so large that it can crush the infra of an AI giant that already serves 500 million weekly active users. That’s a lot of market pull. And with over 20 million paid accounts, it’s not like OpenAI is failing to monetize the inbound.

I’d still bet you $5 that in the next 24 months — hell, 36 months — will be a period of total AI compute paucity and not one of total AI compute superfluity.

Circle’s going public!

Circle, the company behind the USDC stablecoin, is going public. You can find it’s S-1 filing here if you want to read along. Page numbers are included for all charts and tables embedded below.

I interviewed the CEO of Circle last September on TWiST, which you can watch here.

We’ll start with a financial overview, and then dig into the nit and grit of who owns what, and what price Circle could command when it lists.

Is Circle a good business?

Yes.

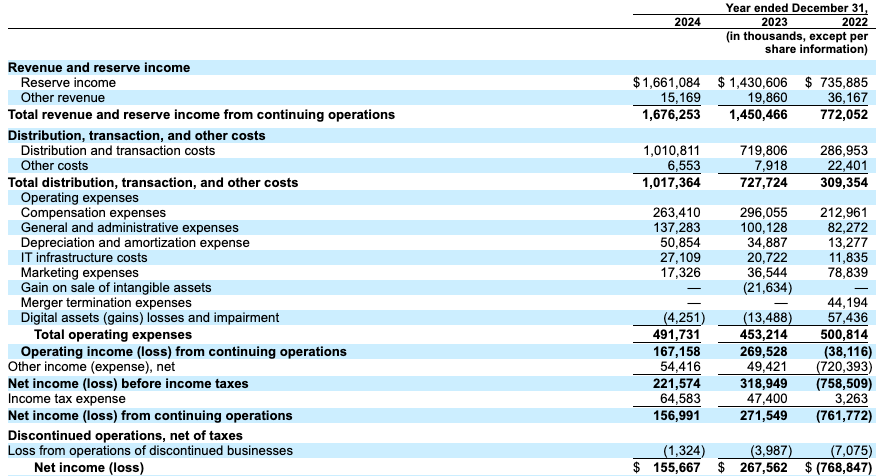

Circle’s revenue grew 15.6% from 2023 to 2024 after growing 88% from 2022 to 2023 (page 104). Circle’s revenues grew faster from 2022 to 2023 than they did last year thanks to cash being worth more. In more practical terms, Circle’s ‘reserve rate of return’ rose from 1.5% in 2022 to 4.7% in 2023 to 5.0% in 2024 (page 98).

Keep in mind that Circle financially operates a bit like a bank. It takes in deposits — people buying its stablecoin — that it holds and collects income against. When users redeem issued stablecoins, the total pile of money that Circle holds declines. So, Circle does best when rates are high (money is worth a lot), and there’s ample net demand for new USDC tokens.

While Circle kept growing even after interest rates stopped rising, the company’s profitability did not. Circle’s net income dropped around 42% last year, compared to the year prior (page 105). Why, if the company’s revenue grew and its opex doesn’t seem excessive? “Total distribution, transaction, and other costs” rose about 40% last year, far greater than Circle’s total revenue.

What are distro, transaction, and other costs at Circle? Let’s talk about Coinbase.