CoreWeave comes pounding back

Hell yeah bring on more IPOs

While the world sorts out the impending tariff mess — the latest is that whatever is announced tomorrow will go into effect “immediately” — there’s good news to report: CoreWeave is ripping higher today.

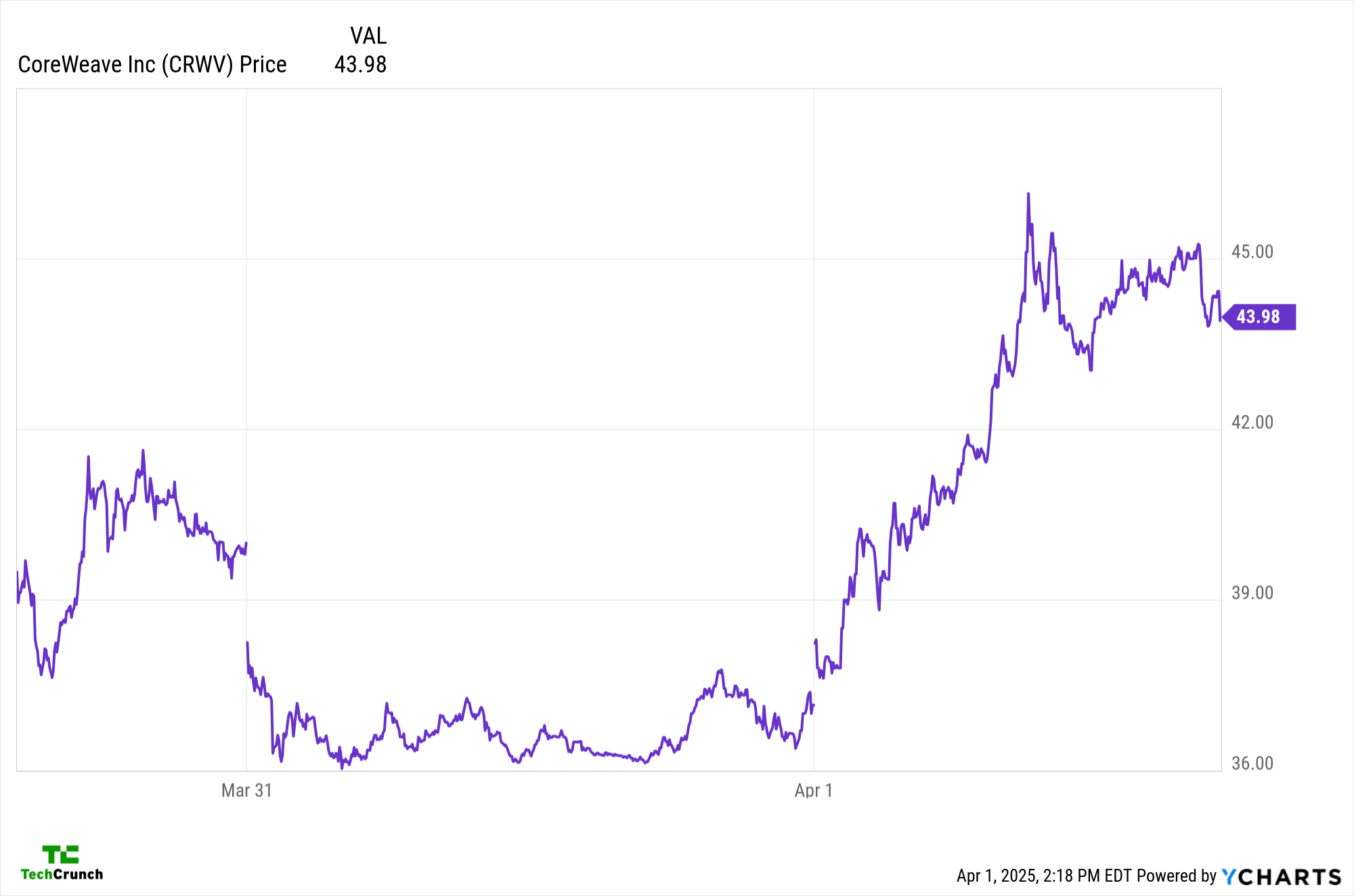

Yes, shares of the GPU neocloud are up around 19% this afternoon, pushing the company comfortably back over its IPO price. Here’s a chart of every minute that CoreWeave has been a publicly traded company:

From a so-so day one, to a Hot Mess day two, to a straight ripper day three. At least going public is never boring.

Of course, we should limit our cheering as CoreWeave remains worth less today than it had hoped to list for. That initial $47 to $55 per share IPO range is more historical quirk than current benchmark, but it’s worth keeping in mind as the market tries to sort out just how to price the company as we await its first earnings report.

For fun, here’s how CoreWeave managed in Q4 2024:

Revenue: $747.4 million (up 28% from Q3 2024)

Operating income: $112.7 million (-4% from Q3 2024)

Interest expense: $149.0 million (+43% from Q3 2024)

Net loss: $51.4 million (∆ N/A)

Given how quickly CoreWeave has grown in the last few quarters, comparing its current market cap of $20.8 billion (Yahoo Finance) against its Q4 revenue converted to a run rate ($2.99 billion) to calculate a run rate multiple (~7x) is unfair.

To be more even-handed, let’s presume that the company managed half the sequential growth that it put up in Q4 in Q1 (14%). With that, we can infer the company exited the last quarter with top line of about $852 million (this number may be far below market expectations, to be clear). That would give it an implied run rate multiple of just over 6x.

I suppose the answer to the question of ‘What is a GPU cloud with mega-growth, reasonable economics, and a lot of debt worth’ is something like ‘around the median ARR multiple for current SaaS companies.’

Harsh? Perhaps, but unlike SaaS revenue that tends to trickle higher over time, GPU cloud revenue can rise — and fall — more quickly.