CoreWeave's IPO disappoints, inflation comes in hot

But not all the news is bad!

Welcome to Cautious Optimism, a newsletter on tech, business, and power.

📈 Trending Up: Damage, after a brutal earthquake in Myanmar … ass-kissing … but why? … friends in high places … bad faith … hypocrisy … saber rattling … whoops … Signal … working the refs …

Becoming default alive: Replit’s Amjad Masad [my recent TWiST interview here] tweeted that getting his company to “default alive” is “so freeing.” Default alive is a Paul Graham term that he defines as the moment when expenses are held flat and current growth trends are up. The startup in question will “make it to profitability on the money they have left.” Congrats, Replit.

📉 Trending Down: GenZ diversification … tattoos … AppLovin … domestic consumption? … free speech … corporate agglomeration … crypto enforcement …

CoreWeave’s IPO

CoreWeave priced its IPO at $40 per share last night, with the company selling 36,590,000 shares and existing shareholders selling 910,000 shares. That’s $1.46 billion for CoreWeave, and $36.4 million for insiders. CoreWeave’s underwriters have the option to purchase another 5,625,000 shares at the company’s IPO price, giving it a total potential raise of $1.69 billion by our math and the company’s official release. (RenCap has a higher figure, oddly.)

No matter, the company is now public, will commence trading today, and has raised enough capital to beat back some of its debts. Debts that at times surpassed CoreWeave’s internal controls.

CoreWeave’s IPO is a letdown, however, in pricing terms. The company had put up an initial range of $47 to $55 per share, far ahead of where the company finally priced.

Recall that Microsoft released some capacity options, which OpenAI snapped up. That brouhaha cast a pall over CoreWeave’s IPO, just as later reports that Nvidia intended to anchor the offering provided a boost.

We’ll get a more accurate report card of CoreWeave’s IPO pricing when it starts to trade, but for now the market has managed to get a unicorn live, and that’s a real accomplishment.

Yesterday CO noted that the rumblings of datacenter overcapacity were picking up steam. On the other hand, OpenAI writes that its new image generating technology proved so popular that it was ‘melting’ its GPUs, forcing the AI leader to limit usage.

You could view CoreWeave’s worth as the first derivative of current market stress for GPUs as the world sorts out AI compute supply and demand.

Inflation

Oof. Here’s the raw data:

“From the preceding month, the PCE price index for February increased 0.3 percent. Excluding food and energy, the PCE price index increased 0.4 percent.”

“From the same month one year ago, the PCE price index for February increased 2.5 percent. Excluding food and energy, the PCE price index increased 2.8 percent from one year ago.”

CNBC reports that the street had expected 0.3% and 0.3% (not 0.3% and 0.4%), and 2.5% for PCE and 2.7% for core PCE (sans food and energy costs). In simple terms, inflation for February came in somewhat above expectations. Stocks are down a bit.

What’s very worrying is that inflation is already above expectations — hopes? — before the impact of recent auto tariffs and whatever comes on April 2nd take their own bite. We could be heading back towards some pretty hot price growth, which is a bummer.

Everyone is worried about SPVs (again)

One way to invest in startups is to raise a bunch of capital for a fund and invest the capital over a set time frame, eventually returning the original cash and profits to your backers when investments exit. Another way to go about it is to simply put your own money into a startup, something done usually early in a startup’s life cycle.

But what if you can’t raise a fund (no new venture firm for you!), and you don’t have the personal capital to effectuate an investment in a company that you want to back (no material angel checks from you!)? You can spin up an SPV.

An SPV, or special purpose vehicle, is a single-shot tool to aggregate capital to invest in a single company. You can think of it as a micro venture-fund with just one investment. In a sense, great. You, the average person, can put a little cash into an SPV and get a micro-slice of some hot company, allowing you to become insufferable during brunch while enjoying the same DPI as the big venture dogs.

There are downsides. Not all SPVs are simple. As with all financial methods, there are good ways to SPV, and bad. Just like going public is great, but going public via a SPAC is not. Both have the same result — a company going public in the IPO and SPAC example, and startups raising capital in the case of SPVs and SPVs — but are rather different.

For example: An early-stage venture fund that wants to defend its ownership percentage in a hot portfolio company could put together an SPV, raising capital from the same backers of its venture fund to continue following-on in the startup in question. That’s logical, above-board, and frankly a very bullish statement on the original investment.

Things can look very different: SPVs can be raised by folks to purchase secondary shares in startups. This is one level of abstraction further than I would be comfortable with. Secondary investors may not receive the same information rights as investors cutting primary checks. Investing on hype instead of known fundamentals is risky.

Or even more different: There are currently layered SPVs in the market. These are essentially SPVs that invest in other SPVs, with fees taking a bite out of both. Yuck.

SPVing into SPVs that are investing into secondary shares feel a bit like synthetic CDOs, right?

The above matters because SPVs are having a moment. Why now? Because there are only so many hot AI companies in the world, and many more dollars want in than the companies are currently raising:

CNBC reports that SPVs are burgeoning in popularity on secondary platforms, and some industry participants are concerned about the rise of retail capital trying to get a crack at AI shares through murky investments.

Altimeter’s Meghan Reynolds recently reported that “SPV Mania” is sweeping the market, with some banks being offered “100 deals in the first 10 weeks of the year” to sell to their clients. The offered transactions include “every sizable deal across PE, RE, Infra, VC, Growth,” often with single or double layers. Ew. Reynolds argues that because “super high quality direct flow from household name GPs” is on offer in some cases, traditional venture fund LPs might skip their normal investing strategy of backing firms, and instead just pick the deals they want.

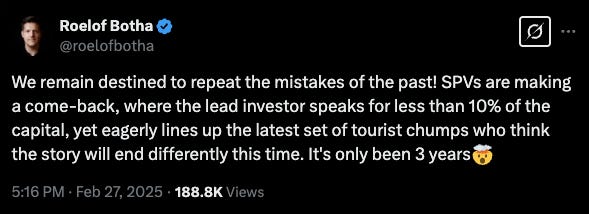

The SPV trend became so pronounced that Sequoia’s Roelof Botha tweeted the following a few weeks back:

What happened three years ago? Venture went a bit nutty, with startups boasting single-digit ARR or less raising at billion-dollar valuations. A lot of those deals went sideways, but were executed at a time when demand for startup equity was so high that SPVs were hot. And now we’re back to seeing tourist capital fight to get a small piece of startups that may prove similarly un-derisked as the 2021/2022 unicorns proved.

I remain an AI bull over a three-year timeline, and a diversified market perspective. SPV at your own risk.