Five takeaways from Klarna's IPO filing

And: It appears that Europe has located its spine (and wallet)

Welcome to Cautious Optimism, a newsletter on tech, business, and power.

Good morning from a rainy Providence. We recorded TWiST last night in a late-night recording for scheduling reasons. Expect that show out this morning. Below we have our usual start of week news bites, drama in HR-land, notes on Europe’s tech push, and Klarna IPO notes to close. Let’s go! — Alex

📈 Trending Up: Consumer credit … in-person interviews … Chinese concerns about Mexican tariffs … constitutional crises … Canada-EU relations … are we now … laser internet … cheaper, faster AI from China … child subsidy …

Consumer goods? Pepsi’s expected deal to buy consumer soda brand poppi is a go. CAVU Consumer Partners led all three known poppi venture rounds, which included — Crunchbase notes — a number of celebrity angels to boot.

📉 Trending Down: Foreign investment in Xinjiang … VOA … Turkey-US relations? … US-China relations …

From the local beat: A “kidney transplant specialist and professor” from Brown Medical “has been deported from the United States, even though she had a valid visa and a court order temporarily blocking her expulsion,” per the New York Times. This, alongside politically-minded expulsions, is bad.

Chew on this: New plans to boost consumption in China are out (link in Mandarin). The “Special Action Plan to Boost Consumption” is long — and quite a lot of it generic, to be clear — but a few things did stand out. From a machine translation:

“Take multiple measures to stabilize the stock market, strengthen strategic force reserves and market stabilization mechanism construction, accelerate the unblocking of medium- and long-term funds.” The Chinese stock market has had a rocky few years, so this makes good sense. A healthier stock market could also help revive Chinese venture capital, which has slowed in recent years.

“Strengthen childbirth and child rearing protection” + “Strengthen educational support” + “Optimize the supply of services for the elderly and children” + “Guarantee the rights and interests of workers to rest and take leave.” Read another way: How can we get people to have more kids?

“Increase support for the trade-in of consumer goods” + “Strengthen the leadership of consumer brands” + “Promote ice and snow consumption.” Simply put: Please, please buy more stuff.

Alongside the Chinese push for greater domestic consumption, domestic retail sales are hardly blowing the doors off, new data indicate.

Drama in the HR-tech world: Rippling, Deel, Gusto, Remote and others have proven that there is room in the market for a number of HR-tech software companies to reach multi-billion dollar valuations. The same cohort has proven that there is also infinite room in the same market for shenanigans and bad blood.

The Times writes that “Rippling on Monday sued Deel, accusing its competitor of hiring a mole in its Dublin office to comb through Rippling’s trade secrets, a scheme that reached its rival’s highest ranks.” Oh yeah, that’s the good stuff.

How about instead of bickering, one of the companies in question fucking goes public?

Europe Rising

I am starting to think that the second Trump administration will prove a key boon for European technology and defense. The overall net economic and political impact of a cantankerous ally across the Atlantic is not clear, but in a few ways we’re seeing positive signs of life on the Continent.

For example, if you wanted to shake up an economic bloc, you might want to sort out:

Bloc-controlled satellite Internet: In late 2024, the EU set in motion a €10.6 billion plan to build a 290 satellite Internet system. In practice, the project means more local capacity, and less reliance on foreign technology and International political harmony.

Bloc-controlled space launch systems: Arianespace’s Ariane 6 rocket pulled off its first commercial flight earlier this year. Again, you want local capacity here to avoid having to ask permission from anyone else to get to space.

That’s just the start. Lately, we’ve seen a number of efforts to greatly bolster European technology pace, prowess, and sovereign capacity:

Datacenter buildouts: France has landed material contracts to build out modern-scale datacenters powered by its ample nuclear power resources. Come for the GPU capacity, stay for the sparkling wine.

A greater focus on building: An AI summit in France detailed a changing focus in the EU away from regulating new technologies as if they were all bite, and towards building the future that might require later regulation. This is a vibes point, but it really does matter.

Increased domestic venture funding: It’s not just Cherry with big goals — the recent Project Europe announcement has me thinking. I got to yammer with its founder Harry Stebbings, but if you don’t have time for the full chat, it’s enough to say that there are real, and loud voices in Europe calling for Europe to stop its North American brain drain.

A focus on linking startups and governments: The Helsing + Mistral tie-up was a big deal. Expect more of the same in the coming quarters as EU nations accelerate defense spending. (I recently added a number of EU defense startups to the TWiST500.)

And, this morning: “European tech industry coalition calls for ‘radical action’ on digital sovereignty — starting with buying local.” TechCrunch has the goods:

Companies spanning areas including cloud, telecoms, defence, along with several regional business and startup associations, have put their names to [a group] letter — which was sent to [European Commission president, Ursula von der Leyen, and the EU’s digital chief, Henna Virkkunen] on Sunday — urging the bloc to switch its tech strategy onto a quasi-war footing by committing to support “sovereign digital infrastructure.”

The plan pushes for reducing reliance on foreign-owned Big Tech by actively fostering development of a so-called “Euro stack.” The European digital infrastructure pitch is not coming out of thin air — a Euro Stack paper written by, among others, the competition economist Cristina Caffarra was published in January fleshing out the strategy in some detail.

Concern from some in Europe is predicated on worries that the United States could turn technology on and off for political reasons. But it’s also about time that Europe had its own technology titans, if we’re moving towards a multipolar world in which the United States intends to cede primacy to a variety of regional powers.

I am not so hopeful by the above changes to publicly herald a new European technology decade. But if I was setting out to shake up the EU scene to boost its technological progress, the above list would be a damn fine set of efforts to start with. Here’s hoping.

Five takeaways from Klarna's IPO filing

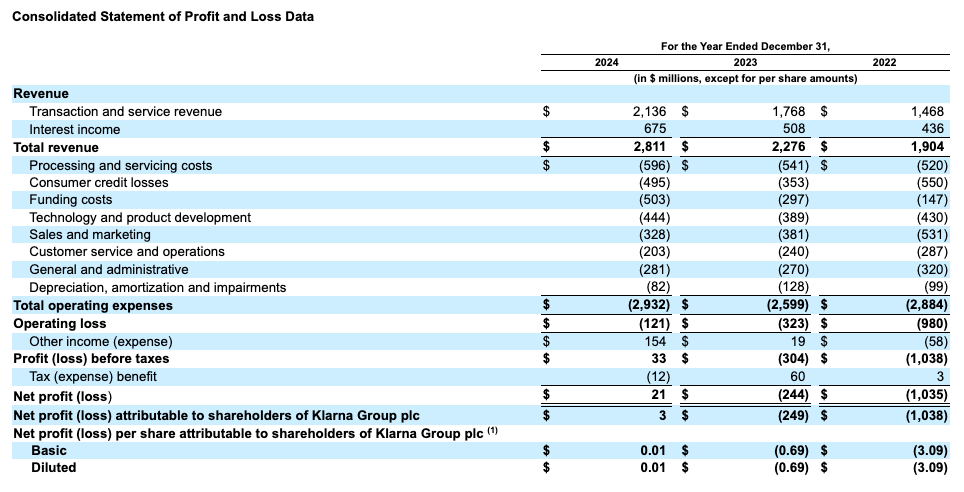

The full F-1 filing is here, bringing the first material IPO to the American markets in 2025. I’ve pasted the income statement below in case you simply want the raw numbers:

Want more? Of course you do! To help, I have distilled the document into five critical points for your consumption:

Klarna’s growth reaccelerated in 2024

Klarna’s buy-now, pay-later (BNPL) business grew 19.5% in 2023, expanding from $1.90 billion in total revenue to $2.28 billion. That’s a pretty solid growth rate for a company at scale, if not exactly scorching. Then, in 2024, Klarna grew a faster 23.5%. Not only is that a much larger figure in raw terms, it’s also a reacceleation, something that you do not see often from larger, more mature businesses.

How did Klarna grow faster last year than the year before?

By growing the number of “Active Klarna Consumers” from +5 million in 2023 (from 79 million to 84 million), to +9 million in 2024 (from 84 million to 93 million).

By expanding the number of purchases that its users make from 10.4x per year in 2022 to 10.9x in 2023 to 11.3x in 2024.

By growing its GMV faster in 2024 (+14%) than in 2023 (+12%), while growing its average revenue per active customer 11% in 2024 after a 13% gain in 2023.

Regardless of your thoughts on consumer fintech companies that charge interest rates in certain cases that you might find alarming, Klarna is firing on all cylinders.

The company’s cost-cutting had huge impact on its profitability

Klarna’s historical costs are fascinating. And often falling.

In 2022 Klarna spent $430 million on technology and R&D. That figure fell to $389 million in 2023 before recovering to $444 million in 2024. That’s a very modest uptick in R&D spend over a multi-year period for a growing company. Not bad.

Even better, Klarna trimmed its sales and marketing costs from $531 million in 2022 to $381 million in 2023 to $328 million in 2024 — all while growing faster!

And Klarna managed to yoink dollars from its “customer service and operations” spend, cutting that line item from $287 million in 2022 to $203 million in 2024.

I mean, what other company has been able to keep cutting core costs while reaccelerating revenue growth. That’s just darn impressive. And helpful. Klarna turned a GAAP net profit in 2024, even if the result was partially boosted by some non-recurring stuff. Klarna really heard the get profitable mantra, and took it to heart.

The company’s major shareholder list is slim

Klarna’s long, and somewhat storied venture capital history did not yield a host of 5%+ owners at the time of its F-1 filing. The company lists Sequoia, Heartland (a Danish billionaire), a former co-founder, and the Commonwealth Bank of Australia as its largest external shareholders.

Sequoia owns 78,812,592 shares, for reference. It could be cruising towards a ten-figure payday in short order.

How much other investors will make is less clear. As is how much of their holding they still, well, hold. I wonder if secondary transactions during Klarna’s life, along with one painful downround lowered some VCs’ effective holdings.

Still, it’s a venture-backed fintech IPO, dammit, and we’re going to celebrate.

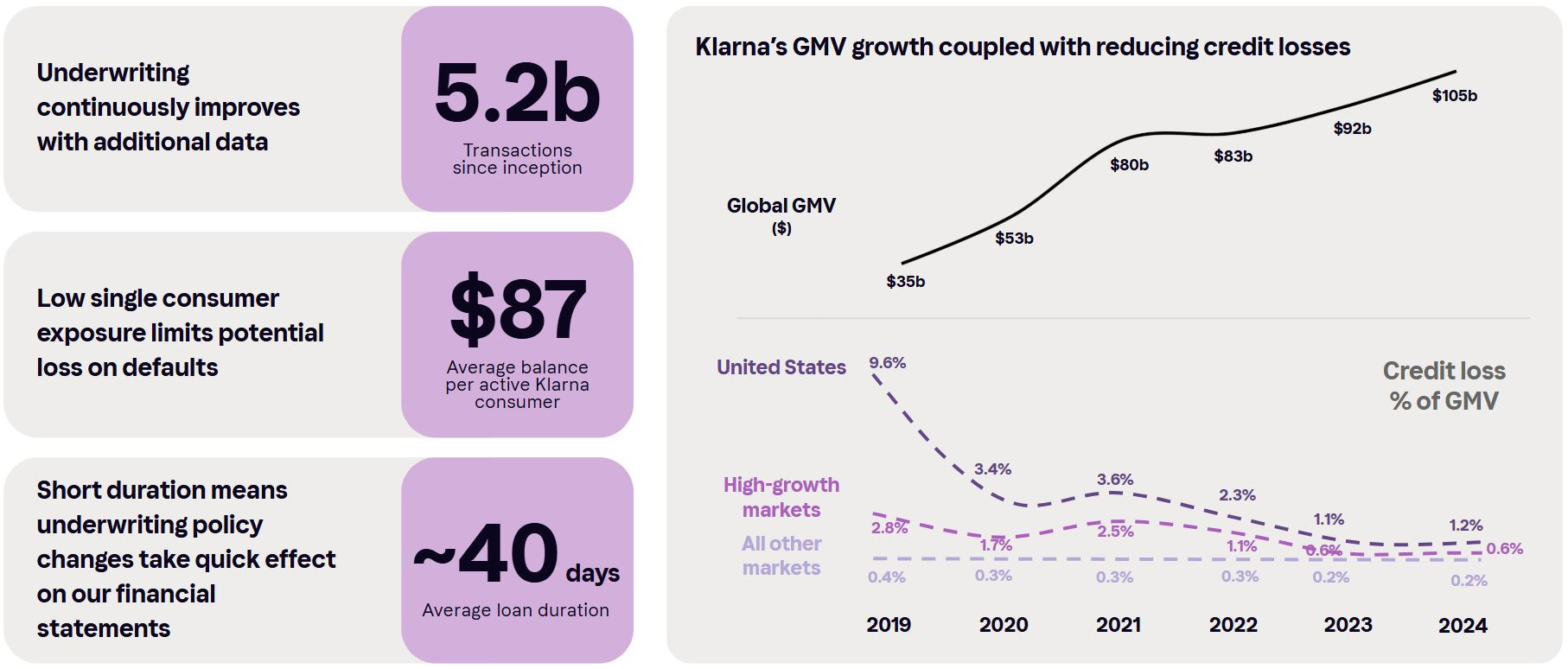

Klarna’s pretty good at avoiding bad debts

Klarna’s not loaning out money to random folks. Indeed, in its IPO filing, Klarna writes that it’s better than its peers at not generating bad debt:

Our underwriting process is optimized for sustainable lending that puts the consumer first. To illustrate the sustainability of our approach, our consumer credit delinquencies at 30 days for the twelve months ended June 30, 2024 were 72% lower than the credit card industry average of 4.2% in the United States based on data from the Federal Reserve Bank of St. Louis.

It’s been a process, as evinced by the following chart:

But one that Klarna has seemingly won.

Klarna’s all in on AI

The cost cutting mentioned above was partially predicated on AI use to allow for more limited human costs. That’s been in the news. Other AI tidbits from the filing that are worth your time include:

“As of August 31, 2024, 96% of our employees used generative AI in their daily work, according to our internal data gathered from OpenAI and our internal AI tools.”

“We use AI to increase productivity within our engineering and operational teams. As of October 2024, 85% of our engineers connected to their work software an AI copilot that can create and review code (based on data exported from the AI copilot).”

“Our legal teams use AI to expedite document review. We also use AI to minimize external vendor costs.”

“Additionally, we operate an internal knowledge chatbot, which we call Kiki, that helps employees find information in real time across internal systems. These internal applications of AI have dramatically increased our average revenue per employee in recent periods.”

That’s AI helping with dev needs, legal needs, cost control, and internal knowledge dissemination. I presume that the Klarna approach will become the norm. Today, it’s a harbinger of how companies are going to approach AI in the future — a method of getting more from individual humans to lower the need for more of them.

We’ll loop back to Klarna when it sets a first price range for its flotation.