Viva la acceleration, and how Medium reset its cap table

Welcome to Cautious Optimism, a newsletter on tech, business, and power. Made just for you.

📈 Trending Up: Boeing … United Fucking Airlines … quitting en masse … competition … surrendering to market forces … Zeal and Ardor …

📉 Trending Down: Buying useless shit … anti-competitive mergers … Adobe, after earnings … interest rates … Chinese corporate formation …

Self-driving accelerates: Shares of Uber are up 5% in pre-market trading after the company reported that, starting in 2025, “Waymo and Uber will bring autonomous ride-hailing to Austin and Atlanta, only on the Uber app.”

The two companies have worked together before, but the last clause of the preceding quote is worth re-reading. Uber continues: “In these cities, Uber will manage and dispatch a fleet of Waymo’s fully autonomous, all-electric Jaguar I-PACE vehicles that will grow to hundreds over time.”

The deal makes sense: Waymo gets a firehose of demand, and Uber derisks its future a bit by getting deeper into self-driving cars now instead of later. What drivers will do in response should prove interesting.

AI accelerates: OpenAI’s new model is a puzzler. It can solve more complicated queries — and it’s both more expensive to use and slower than prior models from the Microsoft vassal. Still, the market was waiting for OpenAI to throw the gauntlet, and here we are.

In the meantime, ChatGPT has 11 million paying subscribers. That’s a lot.

YC accelerates: Well-known startup accelerator Y Combinator is moving to four classes per year (BG). Up from two. That’s a doubling.

The obvious critique of the move is that the last time YC tried to shake up its remit it later retreated.

The obvious argument in favor of YC doing more batches right now is that great startups are often born when times are ‘harder’ in fundraising and valuation terms. For non-AI startups, that’s right now.

How to price AI: I’ve written about how AI-powered enterprise products will get priced before. Back then the answer was we’ll see. Thanks to Salesforce, we now get to see a little bit. Here’s Axios:

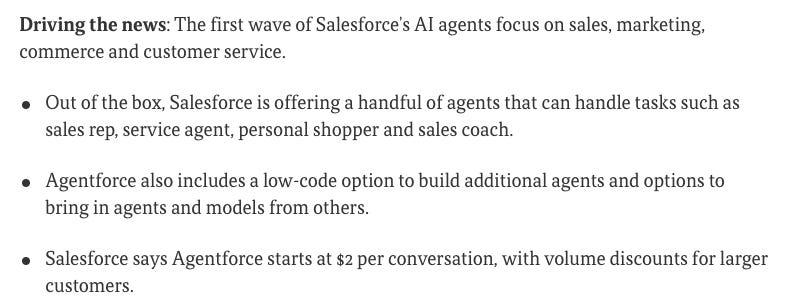

More expensive than you thought? Run a little thought experiment:

What is the average salary of a customer support rep? According to Glassdoor, “Technical Customer Service Representative” salaries in the United States have median pay of $50,000. That’s $25 per hour, not counting healthcare costs and so forth.

How many calls can a rep handle per hour? So long as the number is fewer than 12.5, the Salesforce tech is potentially viable. (Quality of machine responses tbd, of course.)

Mix in a volume discount, and we’re starting to understand just how much digital humans that replace flesh and blood humans will cost. Less, is the answer.

Medium’s recap

Closing the books on our dive into Medium this week, let’s talk about its recapitalization.

As a reminder, CO dug into how Medium retooled its service, found product-market fit, and reached profitability on the back of more than one million paying subscribers. (That last figure, as I am learning from building a partially paywalled media business, is insanely impressive. It’s hard!)

But there was a caveat to the good news: Prior shareholders might not get to enjoy as much upside from Medium’s recovery as this publication initially thought. Why? After a very long and at times meandering life as a private company, the firm reset its cap table.

Medium CEO Tony Stubblebine sent in a detailed response to CO’s queries regarding the financial shakeup. Here’s his letter (emphasis added):

Happy to talk about it. Everything below can be on the record. It's complicated but few companies talk about it and they should so that other entrepreneurs can know how it works. Amazing that there isn't more info given that we just went through an era where a lot of startups had to restructure.

Yes, we did a big financial restructuring in April that converted past-due debt to equity, reset the pref-stack to make the company's equity appealing to new employees, and also opened up a larger equity pool for current and future staff. The end result is that we cleared our debt and the current/future staff has plausibly good equity compensation.The downside is that the conversion of debt and expanded option pool were very dilutive to prior shareholders. But as in nearly all Silicon Valley deals, everyone's equity is more valuable after the restructuring even if it was diluted. That is to say, the equity was probably worth nothing and is now possibly worth something. You can't say that with 100% certainty, but that's an easy to explain position.

These restructurings obviously reflect that we had a very rough patch. But everyone already knows that. The press said it for years and then I started saying it publicly a year ago. Medium was expensive to build, expensive to run, and was losing subscribers in 2022. None of that makes for enterprise value and thus the equity was not worth much, if anything. That's old Medium.

The only thing that's embarrassing for the current version of Medium is that we offered our 120 or so investors rights to participate when the debt converted to equity and fewer than ten of them did. It's hard to puzzle out how much of that is fatigue with how old we are, that we are off trend in an AI era, that it's hard to evaluate momentum when a company is starting below zero versus how much is that they don't think we are doing as well as we think we are.If you want to talk about it, I'd be happy to. The mechanics are pretty interesting. You learn a lot about which VC firms really are pro founder. And the most counter intuitive part to me was why I couldn't do this in year one and had to wait for year two.

First, a thank you to Stubblebine for being open and honest instead of sharing the usual corporate word salad slop we’re accustomed to. I was going to excerpt his missive but decided that it would be more useful for founders and builders to read it in an unabridged fashion. So, there it is.

What I take away from the above is that media remains a very hard venture capital bet. But not one that cannot, at times, benefit from ample external capital. Instead of raising more trad funds, however, if the company decides to, I wonder if an equity crowdfunding campaign would be more useful. Raise some more money and let its existing community buy in, that sort of thing.

I did not buy any Substack stock when it held its own equity crowdfunding event, because the price was too high and it felt unethical to invest in a company that I cover, even if I am far more of a user of Substack than I am a reporter on it. (I suppose that if the chance to buy some Substack stock came up now, I could make my own call as I am off on my own with no one’s rules to follow apart from my own ethical rules; which, to be clear, hew very closely to traditional journalism norms. If you want to offload your Substack shares, alexwrites@protonmail.com for fun.) But it was tempting. Buying shares in something you use always made sense to me.

That’s why, in time, I will buy enough New York Times stock that the dividend payments I would earn could cover the fee I pay to read the paper. Call it a personal perpetual information machine. Until I stop being a journalist, however, it’s index funds for me.

Back to Medium: I hope the above clears the decks. Frankly, I feel like Medium has taken enough of a drubbing for its past strategic pivots. Let’s see how big the company can grow now that it has its house — both product and financial — in order.