We underestimated how much corporate America hates paying developers

And: Google buys Wiz

Welcome to Cautious Optimism, a newsletter on tech, business, and power.

Happy Tuesday! Nvidia’s keynote at its own GTC event kicks off later today. Strap in for a host of news items that will impact a huge swath of the technology industry, both foreign and domestic. Catch our rundown of the Rippling-Deel suit here, and here’s our dig into Klarna’s IPO filing. To work! — Alex

📈 Trending Up: Nerdio … no shit … OSS … American EVs … Tencent Music … German arms … European defense … minefields …

Read of the Day: TechCrunch’s Connie Loizos’ interview with venture investor Aileen Lee discussing orphaned unicorns, board members who step back early, and what LPs might say if they could speak freely.

📉 Trending Down: Baidu’s AI perch … domestic soft power … new Reddit-Google deals? … Tesla stock, again … Chinese venture capital … the Gaza ceasefire …

Quote of the Day: “Respondents to the March CNBC Fed Survey have raised the risk of recession to the highest level in six months, cut their growth forecast for 2025 and raised their inflation outlook.” — Steve Liesman

The AI investment train isn’t slowing down

After reading a number of negative reviews of Devin, a software tool designed to act as a “collaborative AI teammate” for digital engineering work, I am surprised by the news: “Cognition AI Hits $4 Billion Valuation in Deal Led by Lonsdale’s Firm.”

Here, I will note that the two reporters who broke the story — Kate Clark and Katie Roof — are both former members of Equity, my old podcast. Go team!

CO keeps tabs on software forums to ensure that we’re up to date with the current conversation and, dare we say, vibes. Here’s a sampling of what we’ve been reading in recent months.

And yet. Clark and Roof report that Cognition AI, the company behind Devin, is raising nine-figures at a valuation of nearly $4 billion. That’s roughly double its prior valuation of ~$2 billion set amidst an April, 2024 funding round. Founders Fund and Khosla Ventures put up capital in that round. This time, 8VC is leading.

Given that Devin is able to raise so much money at so high a price while market expectations for leading startups include simply incredible revenue growth, we can infer that Cognition and Devin are doing pretty well. Public grousing be damned.

Even more notably, Devin is pulling off a massive fundraise while rivals like Cursor are posting nearly record-setting growth. When the pie is so large that many players can carve out a nice slice, we’re talking about TAM.

I think that we underestimated how much corporate America hated:

Being forced to cater to developer demands when market need was far greater than supply.

Being forced to shell out big dollars for developer talent in today’s more relaxed developer labor market.

If you are looking around your company for costs to cut, your developer salary line item must look like a pretty darn tasty target. Enter AI tools! Devin costs just $500 per month for a “Team” account. That means you can get a full year of Devin’s AI coding help for the cost of what, a summer intern’s stipend?

Shit, why wouldn’t you give it a whirl? At that price point it’s nearly free compared to the running costs of an even Series A startup’s technology team. The question remains what sort of churn we’ll see in coming quarters from Devin and friends, but at least the smart money with deeper insight into historical commercial account retention are doubling down.

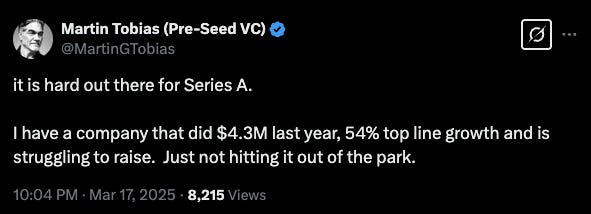

State of Series A

Ed Suh of Alpine Ventures responded that “the unfortunate challenge is 54% is not a great growth rate at A.” Tobias wrote back: “Exactly.”

If you are the Series A company in question, I’d love to talk to you about your growth rate and how you plan to build and raise around it.

All hail cybersecurity

Update after the morning note was sent to its editor: Google confirmed the deal at $32 billion. In cash. The key quote from the release? Google writes that buying Wiz will allow it to provide “an end-to-end security platform for customers, of all types and sizes, in the AI era.”

The big news this morning is that Google is buying Wiz. The FT reports that Google came back to Wiz, a cybersecurity company famous for its simply insane growth pace, with a larger offer.

Google initially tried to buy Wiz for around $23 billion. That offer fell short in the middle of 2024, with the startup deciding to go it alone instead of selling.

That didn’t last, as Google rocked back up with an even larger pile of capital to offer. TechCrunch confirmed the news, pushing the story forward by putting a more precise $32 billion price tag on the deal.

To understand why Wiz is such a prize, and why Google did not give up on buying it, let’s rewind the tape regarding its financial performance:

$100 million ARR in August of 2022, which the company described as a run from zero to nine figures in about 18 months.

$350 million ARR at some point between the end of 2023 and mid-2024.

$500 million ARR in mid-to-late 2024.

Plans for $1 billion ARR in 2025.

If you are a company like Google, hellbent on diversifying your revenue streams as legacy incomes become harder to juice — if Google Search adds any more ads, I swear the entire first page of results offered could become inorganic — picking up leading assets that plug into your plan are very attractive. As Google is building out its cloud business while fighting for AI dominance, adding a winning cybersecurity org to the mix seems like a well-rounded choice.

Going back in time, did Wiz-Google Round 1 die on the vine over price, or something else? The FT writes that the original deal “collapsed after some of the cyber security company’s directors and investors became worried about antitrust hurdles.” In short, blame the Biden administration in general and former FTC head Lina Khan in particular? I wonder.

The second Trump administration is hardly backing away — yet, at least — from Biden-era views on antitrust, and is critical of Big Tech in its own right. The deal might have an easier run at being passed through by regulators, but I am not entirely certain that it will. From that perspective, the Wiz-Google deal should prove a good test case for the current antitrust sentiment in D.C. If the Juniper-HPE mess was more fluke than precedent.

I would have gone the Figma route, frankly. Adobe tried to buy the smaller company, and the deal had a $1 billion kill clause. Eventually, the two companies gave up on the deal after running afoul of global regulators. And Figma got a flat billy for free! Sure, it had some distraction to deal with while the deal sat in limbo, but a free billion?

Wiz could have negotiated something similar, yeah? Nothing as nice as another $10 billion or so worth of extra value by waiting, but if we hold to that logic, Wiz should wait another year to sell so that it can keep growing!

No matter the back-and-forth, we’re now feasting off a massive venture-backed exit as we also count down to not one, but two IPOs. It’s a super great way to end the quarter.

Makes sense. Developers weren't the most cooperative bunch to manage. You want to make money and the junior developer is trying to sneaking the latest JS hotness into your codebase. Misaligned priorities.

And let's not forget, Devin never start his sentences with "actually"...